A Laboring Day for the Job Market

Last Week in Review: The Jobs Report for August was released. How did home loan rates react?

Forecast for the Week: The second half of the week heats up, with news on inflation, retail sales, consumer sentiment and more. Plus, the Fed meets!

View: An upcoming fee increase is going to impact home loans. See important details below.

Author Bio: Rob Alley earned a bachelors degree at Virginia Tech, in Blacksburg, VA in Biology. Rob Alley consults with homeowners regarding Real Estate transactions and speciliazes in listing and selling Charlottesville Real Estate. Realtor/Owner of Virginia Real Estate Solutions at RE/MAX Assured Properties

Charlottesville Real Estate Experts

Share on Facebook

Forecast for the Week: The second half of the week heats up, with news on inflation, retail sales, consumer sentiment and more. Plus, the Fed meets!

View: An upcoming fee increase is going to impact home loans. See important details below.

| Last Week in Review |

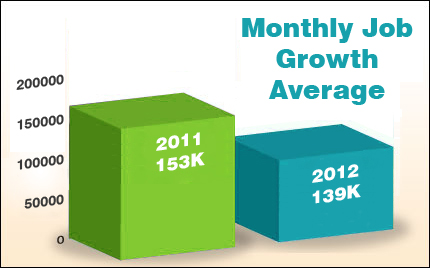

“Everybody’s working for the weekend.” That 1980’s ditty by the band Loverboy applies to fewer people than expected these days, after the Labor Department released its Jobs Report for August. Read on for the details, and what they mean for home loan rates. On Friday, the Labor Department revealed that 96,000 jobs were created in August. This was below expectations of 130,000 and well below the elevated expectations after the surprisingly good ADP report for August. Only 103,000 private sector jobs were created, well below expectations, while government job losses were in line with expectations. Downward revisions to June's and July’s job numbers, which erased an additional 41,000 jobs from what was previously reported, added to the negative tone of the report. On Friday, the Labor Department revealed that 96,000 jobs were created in August. This was below expectations of 130,000 and well below the elevated expectations after the surprisingly good ADP report for August. Only 103,000 private sector jobs were created, well below expectations, while government job losses were in line with expectations. Downward revisions to June's and July’s job numbers, which erased an additional 41,000 jobs from what was previously reported, added to the negative tone of the report.The Unemployment Rate, also a major headline, dropped from 8.3% to 8.1%. How did this happen with the weaker than expected headline job creations reading? The civilian labor force shrank by nearly 400,000. The shrinkage in the labor force is clearly seen in the Labor Force Participation Rate (LFPR), which reached its lowest level since early 1981. This is significant because if less people are "participating" or have a job, this makes it more difficult to pay down our debt. What does all of this mean for home loan rates? There is a very real possibility that the Fed will announce further stimulus measures (known as Quantitative Easing or QE3) at the Fed Meeting on Thursday, September 13th at 12:30pm ET. It’s important to note that once an official announcement of QE3 is made, Bonds and home loan rates could suffer as Stocks would likely rally. However, the weak economic data here and the continued problems in Europe mean that investors will likely still see our Bonds as a safe haven for their money. And as home loan rates are tied to Mortgage Bonds, this would help home loan rates in the process. We saw some evidence of this last week, as Bonds and home loan rates rallied Friday after the weaker than expected Jobs Report was released. The bottom line is that now is a great time to consider a home purchase or refinance, as home loan rates remain near historic lows.Let me know if I can answer any questions at all for you or your clients. |

| Forecast for the Week |

| The Mortgage Market Guide View... |

| Fee Increase to Impact Home Loans The Federal Housing Finance Agency (FHFA) has again increased the guarantee fee they charge to lenders delivering loans to Fannie Mae and Freddie Mac. This is important to know, as this increase has a rippling effect that will impact the cost of mortgage financing. Here's what's happening and what it means to home loan rates: What exactly is this "g-fee"? The guarantee fee or "g-fee" is an amount charged by mortgage-backed securities (MBS) providers, like Freddie Mac and Fannie Mae, to help protect against credit-related losses in the overall mortgage portfolio. In other words, it acts a lot like insurance and helps lower the overall risk...which means home loans can be offered at terrific interest rates to borrowers that have good – but not perfect – credit. What exactly is the impact of the rate increase? The increase will impact loans with different amortizations in different ways. For example, for a $200,000 home loan, the increased g-fee (assuming a .125% increase in rate) would equate to $250 more per year in interest, or $7,500 more over 30 years. Someone buying or refinancing a home can certainly choose to buy down the cost with cash up front – but most folks will not do this. Why is the guarantee fee being increased? FHFA has increased the guarantee fee to collect more revenue to enhance the safety and soundness of the Government Sponsored Enterprises (GSEs), and perhaps indirectly encourage private firms to participate in the mortgage market. Who will this impact? The change will impact all new borrowers using Fannie Mae and Freddie Mac loans. When will it start? Officially, the increase to guarantee fees will begin on December 1, 2012. However, Fannie Mae will also be making adjustments to pricing for those loans that are committed on or after November 1, 2012. It’s important to note that the increase is already being seen in rate sheets right now, since home loans being originated now will likely not be closed, pooled and securitized until December and therefore will need the increased g-fee priced in earlier. The bottom line is that the g-fees will be going up...and this will impact homebuyers looking to obtain a home loan through Fannie Mae and Freddie Mac.

Economic Calendar for the Week of September 10 - September 14

|

Charlottesville Real Estate Experts

Share on Facebook

Comments

Post a Comment